File:IllustrationCentralTheorem.png · Wikimedia Commons · See Wikimedia Commons

Key facts

- Type

- Theorem

- Field

- Probability theory

- Statement

- The scaled sum of a sequence of i.i.d. random variables with finite positive variance converges in distribution to the normal distribution .

- Generalizations

- Lindeberg's CLT

via Wikipedia infobox

Wikidata facts

- Image

- CLTBinomConvergence.svg

Show 2 more facts

- short name

- CLT

- Commons category

- Central limit theorem

Sources (3)

via Wikidata · CC0

~40 min read

Article

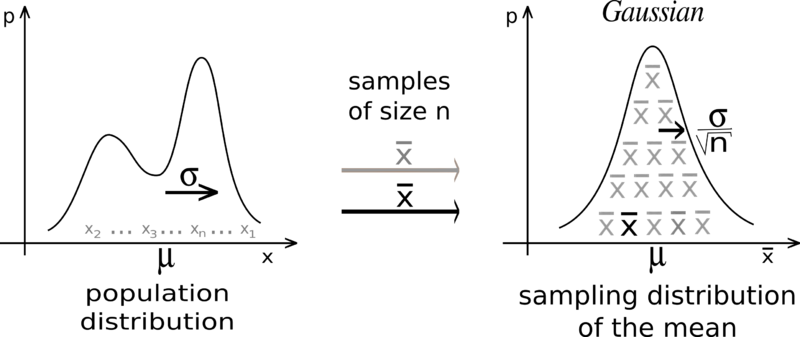

In probability theory, the central limit theorem (CLT) states that, under appropriate conditions, the distribution of a normalized version of the sample mean converges to a standard normal distribution. This holds even if the original variables themselves are not normally distributed. There are several versions of the CLT, each applying in the context of different conditions.

The theorem is a key concept in probability theory because it implies that probabilistic and statistical methods that work for normal distributions can be applicable to many problems involving other types of distributions.

Gallery (3)

Connections

convergence of random variables

Entity

median

Entity

independent and identically distributed random variables

Entity

resampling

Entity

random variable

Entity

probability distribution

Entity

expectation

Entity

law of large numbers

Entity

probability density function

Entity

statistical population

Entity

dependent and independent variables

Entity

Pearson product-moment correlation coefficient

Entity

Sergei Natanovich Bernstein

Entity

power of a test

Entity

errors and residuals

Entity

trend estimation

Entity

demographic statistics

Entity

statistics

Entity

Alan Turing

Entity

International Standard Book Number

Entity